Are you Prepared for Minnesota's Paid Family Medical Leave Program?

Insights Firm Updates Young ProfessionalBrennan McCarthy, CFP®

Minnesota’s new Paid Family Medical Leave (PFML) passed with some controversy last year, but it opened some decent options for new parents in terms of paid leave time.

But if you and your spouse are both high earners, here's what you need to understand before you count on it: the program was designed with the average worker in mind. And the average worker earns a lot less than you do.

What Does Paid Family Medical Leave (PMFL) Actually Cover?

Minnesota’s leave landscape has gotten more complicated in recent years. There are now two separate state programs that often get conflated:

Earned Sick and Safe Time (ESST) is the state's paid sick leave law, which went into effect in 2024. It accrues at one hour for every 30 hours worked, up to 48 hours per year. It can be used for illness, medical appointments, and certain family caregiving needs — and yes, it can be used in small increments around a birth or recovery. But at a maximum of 48 hours annually, it's a minor factor in the overall parental leave picture.

Minnesota Paid Family and Medical Leave (PFML) is the bigger program, and the one that matters most for new parents. Starting in 2026, it provides up to 12 weeks of bonding leave after the arrival of a new child. If new mom also qualifies for pregnancy-related medical leave, the combined total can reach up to 20 weeks for her. The program runs concurrently with federal FMLA where applicable, and it's funded through a shared payroll premium of 0.88% of wages, split between employer and employee.

What will you get from the State?

There are 3 tiers to the program, but most moderate and high earners will be limited by the cap.

Tier 1: If your average annual earnings are $37,000/year or less ($711.50/week), you’ll receive 90% income replacement for the 12 week period.

Tier 2: If your average annual earnings are between $37,000-$74,000/year ($711.50-$1,423/week), you’ll receive 66% income replacement for the 12 week period.

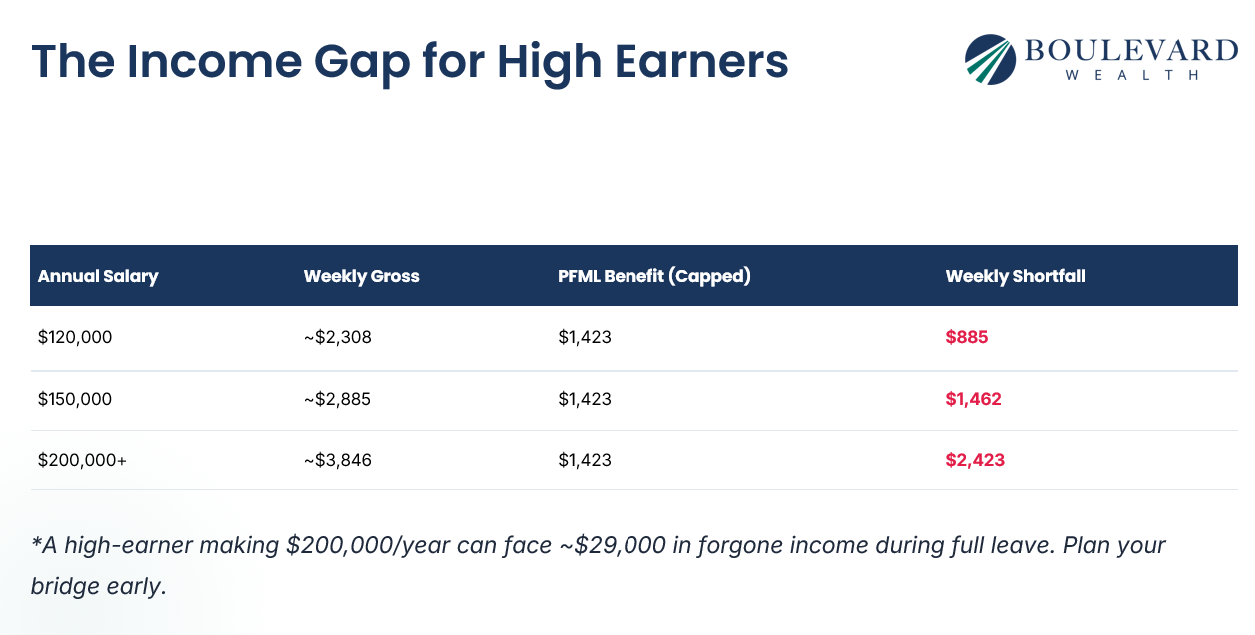

Tier 3: If your average annual earnings are above $74,000/year ($1,423/week), you’ll receive 55% income replacement for the 12 week period. But the benefit is maxed out at $1,423/week (applies to those earning $135,000/year or more).

How does Minnesota Calculate your Benefit?

The state doesn’t simply look at your current paycheck or a recent tax return. It’s based off the quarter (3-month period) where you earned the most over the past year. So, if your leave begins in October 2026, Minnesota will look at your wages earned from July 2025 – June 2026; and take the “high quarter” from that period.

In many cases, this is an important detail that works against the mid-to-high earner. If you had a large one-time bonus last year, your earnings will be based on that quarter, and can push the worker into a lower payout tier, reducing the overall benefit from the program.

High Earners Don't Fare as Well through the PFML Program

For people who planned well in advance and want to take as much time on parental leave with their baby as possible, the PMFL program is a decent option. But given how the income replacement scale look, many high earners find the reduction in income (receiving $1,423/week) is too much to swallow.

For someone earning $60,000 a year, that cap is largely irrelevant. Their weekly gross is around $1,154 — below the ceiling — so PFML covers a substantial portion of their income.

For someone earning $120,000 or $150,000 a year? The math looks very different.

How Much Income will you Lose if you Opt into the Program?

Consider a an individual earning $200,000 per year. Here's what PFML actually replaces — and what it doesn't:

If this high earner takes his/her full 12 weeks of bonding leave, they'll face roughly $29,000 in forgone income over a 12 week period — and that's before accounting for taxes owed on PFML benefits received, or the stack of new expenses arriving at the same time: medical bills, baby gear, and in many cases, a daycare deposit due before the baby even comes home.

This isn't a flaw in the program. PFML is structured intentionally as a progressive benefit — it replaces a higher percentage of income for lower earners by design. Since it’s designed to provide a greater benefit to lower earners, high earners will have to calculate whether taking the benefit (and full leave) is worth it.

Do you know how much your Employer will Supplement (or Replace)?

One important variable: your employer may allow you to supplement PFML benefits with accrued PTO, sick time, or a separate employer-paid parental leave policy. If your company offers robust paid parental leave on top of PFML, your actual income gap could be much smaller than the numbers above suggest.

This is worth a direct conversation with HR well before your due date. It’s important to know:

- Does your company offer employer-paid parental leave, and does it run alongside or separately from PFML?

- Can you use PTO or sick time to top off your PFML benefit to get closer to my full salary?

- What is the process and timeline for applying for PFML benefits through the state?

Getting clear answers to these questions early gives you an accurate picture of what your household income will actually look like during leave — which is the number you need to plan around.

When Should you Start the PFML Process?

The state accepts applications up to 60 days before your leave is expected to start, and for a planned event like a due date, that early window is worth using. The applications can take a month to process once submitted, so applying early gives the state time to verify your wages, confirm eligibility, and resolve any issues before your leave actually begins — rather than scrambling after the baby has arrived.

Build the Bridge Yourself

If your employer doesn't supplement PFML — or only does so partially — the income gap is real, and it may not make sense to use the program. We’re often seeing cases where there are 2 high earners in a family, the mom will use the full 12-week period, and the dad will simply use whatever his company benefit is (which is usually shorter) to avoid missing out on a substantial amount of earnings.

The most straightforward approach is the same one that works for daycare savings: if you plan to use the program, work through a calculation NOW so you know how much in forgone earnings you will have over that time. Then, start saving today so you have at least that amount of excess cash sitting in a savings account by the time benefits start. If your household is looking at $29,000 in reduced income over a combined leave period, and you have nine months before your due date, that's roughly $3,100 per month to fully close the gap — or a smaller amount if you're willing to partially self-fund and partially absorb the difference through temporary spending adjustments.

The goal is to avoid unexpected emergencies because you weren’t prepared for an income gap — pulling from retirement accounts, going into debt, cutting savings — while you're sleep-deprived and adjusting to a newborn.

The Bottom Line

Minnesota PFML is a meaningful step forward for working families in this state, and for most workers, it delivers real value. But "most workers" doesn’t work if you don’t fit that category. If you and your spouse are both earning six figures, the program was never designed to make you whole. The good news is that the gap can be calculated and planned around. The earlier you start, the less painful it is. Make sure you run your numbers, have the conversation with HR, and start saving ASAP to prepare for it.